Investing Strategies for 2025

Derisking Likely Outcomes

There are several strategies that come down to a likely but uncertain outcome actually happening and the stock reacting positively to the realized improved business.

Producer Expanding Production

In 2025 I invested in 5 miners, the only 2 with positive returns expanded production during the time I held them. I'm going to graduate this to a strategy with it's own summary page on the site.

Part of this is the de-risking premium. Part of it is the market tends to project the present indefinitely; it's backwards looking and not forward looking.

Another part is that companies that can re-invest cashflow from earnings into things that have a high return on capital can compound returns.

I don't have perfect fits for this strategy now, but am looking.

$HCC Warrior Met Coal Blue Creek won't be in production in 2025, but I'm in early based on valuation.

$LAAC Lithium Argentina is in the ugly part of ramp after first pour but before they are hitting nameplate capacity, their expansion projects won't get financed in the current commodity environment.

Looking at but no position in Aura Minerals, Calibre Mining, & Silvercorp.

Pre-Production Sweet Spot

Financed and permitted. Hold until first pour or maybe declaration of commercial production.

$MAU.V Montage

$ERD.TO Erdene

$RIO.V Rio2

I aim to have these be half positions and to try to ignore them as much as possible. I'm looking for more.

Post Discovery Explorers

I'm looking for projects that can be Tier 1. This strategy is super risky and requires a lot of time investment. Pretty common to have -75% returns, or +200%. But at least there is a there there. Having drill results and sharing analysis with other investors you respect I think it's possible to increase the likelyhood of being right here so that the winners will outnumber the losers and the overall strategy can have positive expected returns.

In 2024 I hit on 2 of 3 of these, or 2 of 4 if you include lithium, and the third I think it's too early to say that was a miss.

Going into 2025 I have 2 positions here and have my ear to the ground looking for more.

$ARIC.V Awale

$QTWO.V Q2 Metals

Royalty

I thought in 2024 the mid-tier precious royalty companies would get taken out, and I was wrong. I still think it could happen in 2025. Even if they don't get bought out the valuations are more compelling for me than buying the big 4 ($FNV, $WPM, $RGLD, $TFPM). I own $ELE.V, $SAND, $OR, & $EMX, though an argument could be made that Elemental and EMX are becoming more and more non-precious. I'm starting to look at Metalla despite my previous reservations; their assets do look compelling here.

I'm also seeing value in pre-revenue royalties, which fits my de-risking likely outcomes as an investment strategy. I'm seeing the non-precious royalty companies trading at a discount and am starting to do more deep dives on them.

$LIRC.TO and $DRR.AX are in my portfolio. Ecora, Altius, Labrador Iron are getting some deeper dives on my shortlist. I'm also considering Franco due to possible resolution of Cobre Panama.

Project Generators

$KLD.V Kenorland is currently my only project generator position, this looks like a long term hold for me with good management just continuing to execute well. I'd like to have more project generators in my portfolio. I'm taking another look at previous holding Globex and find Mundoro intriguing.

Network Effects at Reasonable Valuations

$YELP

$CHL.AX

I like to hold network effects companies, especially two sided marketplaces. Ideally ones that haven't completely saturated their markets. Meta has saturated the market unless they can get virtual reality to take off. eBay saturated their markets. I also don't like to overpay, think single digit multiple to sales not double digit multiples to sales. I'm on the hunt for more of these.

One getting another look is Abaxx technologies.

Differentiated Specialty Finance

$AER - I wish I had a whole portfolio of companies like this. Just smart deployment of capital. Once a quarter I look at their quarterlies and other than that I don't spend any time on it. They are up 55% in the last 5 years, which included COVID shutting down all air travel causing a 70% drawdown in the stock price and Russia stealing a bunch of their planes when the war broke out.

The non-differentiated ones tend to be in real-estate. There are some real-estate ones that are differentiated. Cellphone tower companies are great businesses for example, but they are recognized as great and their stocks trade at astronomical valuations. Data center companies are pretty awesome, but trade at nosebleed valuations.

Regression To The Mean

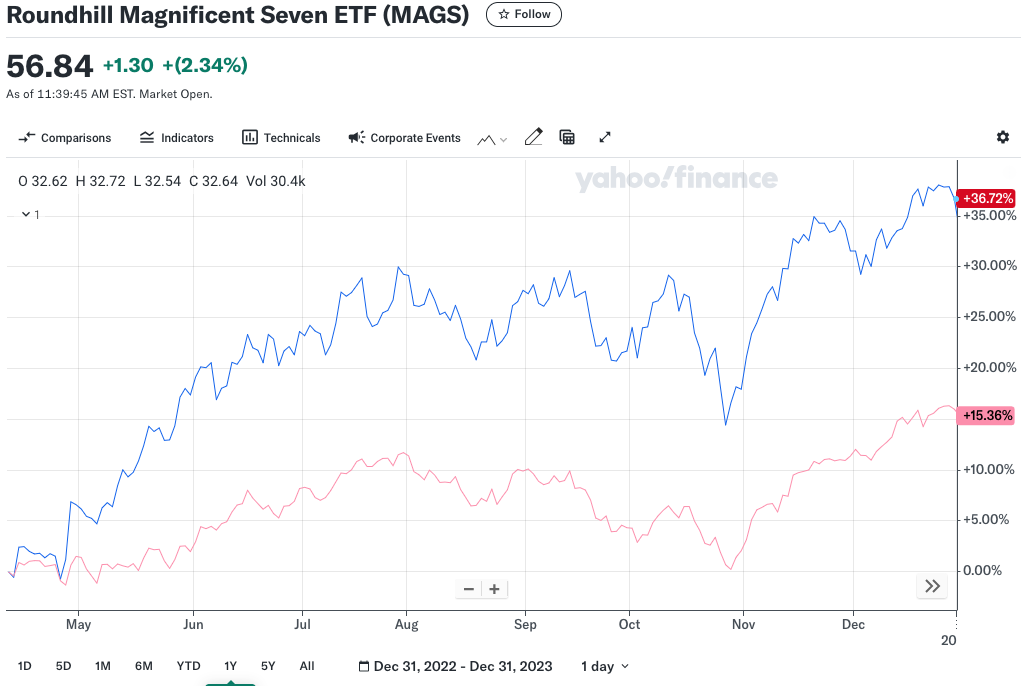

I'm old enough that I was around for the dot com bubble and bust. I invested in eToys. It turns out this internet thing was real and did stick around, but many of those companies including eToys went bust. Even some that stayed around and were the business winners like Cisco never really regained their bubble highs.

As I think about AI it feels exactly the same. Lots of companies rushing to pour as much money as they can. Not clear that there are successful business models there yet, or who the winners will be. This AI push has propped up the S&P500 generally and the MAG7 specifically. You can see the last 2 years of the Mag7 in blue and the S&P500 in pink for 2024 and 2023:

Meanwhile what's been ignored are small, value, and foreign equities. Will 2025 be the year of regression to the mean, who knows; but that's the way I'm placing my bets.

Mexico

$EWW or $FLMX. $FLMX has a 0.19% fee instead of 0.50% for $EWW but the bid/ask spread is 0.25% instead of 0.042%. I went with $EWW to not overthink it, but I bet $FLMX is more efficient if you only trade at open/close or plan to have a multi-year holding period.

At the end of the year it had a P/E of 11.46 and P/B of 1.67, which is pretty cheap. -30.46% in 2024, so the dispersion from the S&P500 is pretty stark. -20%+ was from the Sheinbaum election and the rest from the Trump election. Sheinbaum is rolling back the 2013 energy reforms and Trump is threatening tarrifs, I'm betting neither will be as bad in practice as it seems. $EWW since inception has returned 7.85% annualized but the 10 year is -0.35%.

Overall the composition is a lot of pretty stable high quality companies. Airports, Walmart Mexico, consumer staples, Cemex, Groupo Mexico, banks, cellphone providers. Not fast growing tech companies but companies with real businesses and wide moats.

Brazil

$EWZ was -35% in 2024. Some of this is company specific, VALE got hit by lower iron ore commodity prices. Petrobras has constantly been meddled with by the government. $EWZ has returned 5.29% since inception, but -0.35% over the last 5 years and 0.70% over the last 10 years. It's currently trading at a P/E of 7.56 and a P/B of 1.44. Some of that is justified with more cyclicals in the index, but at some point cheap is cheap.

$EWZS avoids the commodity exposure of VALE and Petrobras, but the quality of Brazilian small caps brings it's own set of challenges.

Other Out of Favor ETFs

$VTWO Vanguard Russell 2000

$MYLD Cambria Micro & Small Shareholder Yield

$VWO Vanguard Emerging Markets

$IEFA iShares Core MSCI EAFE

These aren't as dramatically undervalued as Mexico and Brazil, but in a quick tilt away from US large cap growth these are some others I'm looking at. Diversification and rebalancing is a kind of free lunch.

You can see some of the historic .com level imbalances we have in large vs small, US vs foreign, and growth vs value in this awesome post:

Charlie Bilello

Charlie Bilello

Other

My idea cupbord is pretty bare. If you have some ideas share them with me on the former bird app, DMs are open. https://x.com/latinmines