Lithium Koala Thoughts

The Koala posted a nice blog post on Lithium drawing comparisons to Iron Ore 20 years ago. I thought it was great and that I'd add a few thoughts of my own.

Pegmatites/Spodumene

The Koala nailed this. Like iron the prize is large deposits with high grade and good infrastructure. These are the projects that can sustain through cycles. Though last cycle when Lithium Carbonate and Hydroxide hit $3,000/ton a lot of them weren't competitive with brine evaporation pond producers and closed. They were the marginal producers at the top end of the cost curve. Today with lithium at $78,000/ton it's hard to imagine these large scale hard rock mines ever seeing the price drop below their cost of production again.

There will be marginal producers in hard rock. The koala's numbers are probably the line. Less than 100Mt resource or less than 1% Li2O puts a project as a marginal producer. Tier 1 would be at least 200Mt and at least 1.1% Li2O.

Some of these marginal producers might go into production in special circumstances, say if they are chemically similar to other feedstocks going to a nearby processing plant or if they are particularly close to surface and have great infrastructure. Someday there will be pullbacks in lithium price and you don't want to be holding one of the marginal producers in that environment. You can have a sandbox worth of pegmatite and produce a 6% spod con that gets trucked hundreds of miles to port and make money at $78k/t but if it drops back down to whatever the long term incentive price is or below that suddenly your customers start being picky and your costs start to matter.

Sedimentary Lithium

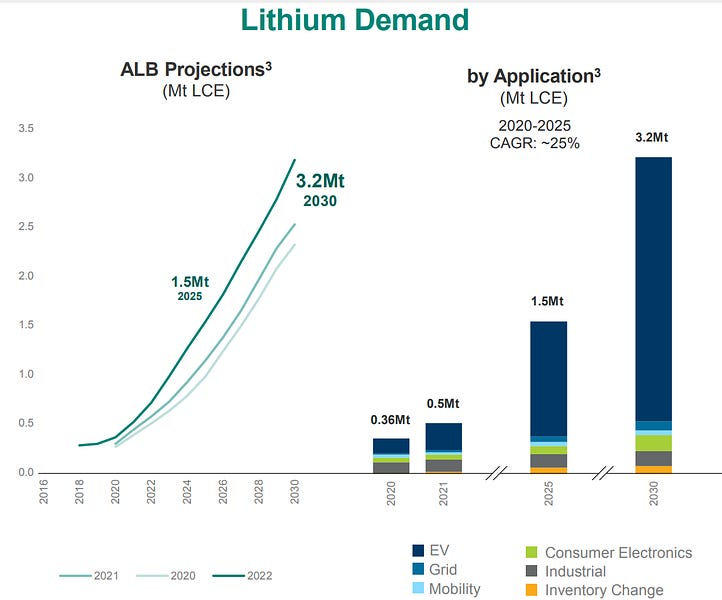

Fortescue turned 56-68% iron that was previously considered dirt into being a 4th major. The parallels to sedimentary lithium are striking.

Sedimentary Lithium, sometimes called lithium clays, is a huge potential source. Greenbushes may be the largest hard rock deposit at 360Mt * .015 Li2O * 2.473 LCE/Li20= 13.35 Mt LCE, but Ganfeng's (formerly Bacanora) Sonora Lithium is 8.8Mt LCE and Lithium Americas Thacker Pass is even bigger at 13.7Mt LCE.

Of course we are comparing apples and oranges as to date no large scale sedimentary lithium deposits have gone into volume production. The most advanced ones have had large scale pilot plants.

I discussed Sonora and Thacker pass a bit in my previous article on Trident Royalties, who I have a long position in due to their royalties on Thacker Pass and Sonora.

Like pegmatities what will seperate successful sedimentary projects from the pack will be scale, grade, and access to infrastructure. Thacker Pass relies on the US not being stupid in permitting, which is a tough bet to make right now. Sonora relies on the Mexican government not to nationalize it, which is another tough bet.

DLE

Let's start out by saying not all DLE projects will be successful. It's not a magic wand you wave that fixes all the projects problems. E3 Metals has some Alberta oil & gas field brine aquifers with 75 parts per million lithium compared to lithium brine typically in the 500-1500 range. Grade still matters in DLE.

It also remains to be seen if the different DLE technologies can work at production scale, and if they can work at production scale on any particular brine.

However, if it does work, wow some of these things will be huge. The Smackover acquifer in Arkansas alone could provide probably half the world's lithium. Standard Lithium is operating a large scale pilot plant there now and has some pretty big resource numbers across its two projects. Those two projects cover a tiny portion of the overall smackover acquifer.

Most of the other DLE projects are in desert areas that would naturally lend themselves to evaporation ponds, but for one reason or other can't use evaporation ponds. Maybe they don't have adequate fresh water supply, have to re-inject brine into the ground to maintain acquifer levels, have deleterious elements, or other problems. Some of these may get saved by DLE, but it's almost certain that some will never overcome the technical challenges and will remain trapped resources.

Lepidolite

It turns out there is a lot of lithium in the world in a lithium mica called lepidolite. To date nobody has mined it because it is hard to process. It's often found in pegmatite mines and is even often moved as waste material. There's a company named Lepidico building a processing plant and a small mine to prove it can be processed at commerical scale. It's worth keeping an eye on as the technology could be added on to existing hard rock mining operations and could open up new deposits. Lepidico's Karibib project is pretty small presently, so any investment is a long term bet on the technology more than the resource.

Full Disclosure

As of the time of publication of this article..

I have no past or current positions in Lithium Americas, Baccanora, Gangfeng.

I have had long positions in the past in Standard Lithium, E3 Metals, and in Electric Royalties (who have royalties covering some of the projects mentioned)

I have a current long position in Trident Royalties

All positions past and present mentioned above were long positions purchased in the public market. I have received no sponsorship for this article.