Renewable Royalties Part 1

Altius Royalties is a company I admire with great assets and great management. My napkin pass at their assets says their mining royalties are probably undervalued. But a lot of their cash is getting reinvested in renewable energy (wind and solar in this case) royalties. I've been trying to figure out the value drivers for these royalties and if I think they are a good investment.

Brian Dalton recently gave this interview, it's worth watching, he's a smart guy talking about a great company.

The point he made that I hadn't considered is that these wind and solar farms when the equipment wears out will already have the site and the interconnect and will presumably be in some of the windier/sunnier locations. It's way easier and cheaper to replace this equipment than to build a new greenfield solar/wind farm. Thus, it's very likely that either the equipment will outlast its design lifetime with extra maintenance or it will be replaced and maybe upgraded. Maybe it is best to think of these not as depleting assets, but as perpetual assets.

Royalties on perpetual assets does sound good. So let's take a look at the most recent deal I could find from Altius Renewables.

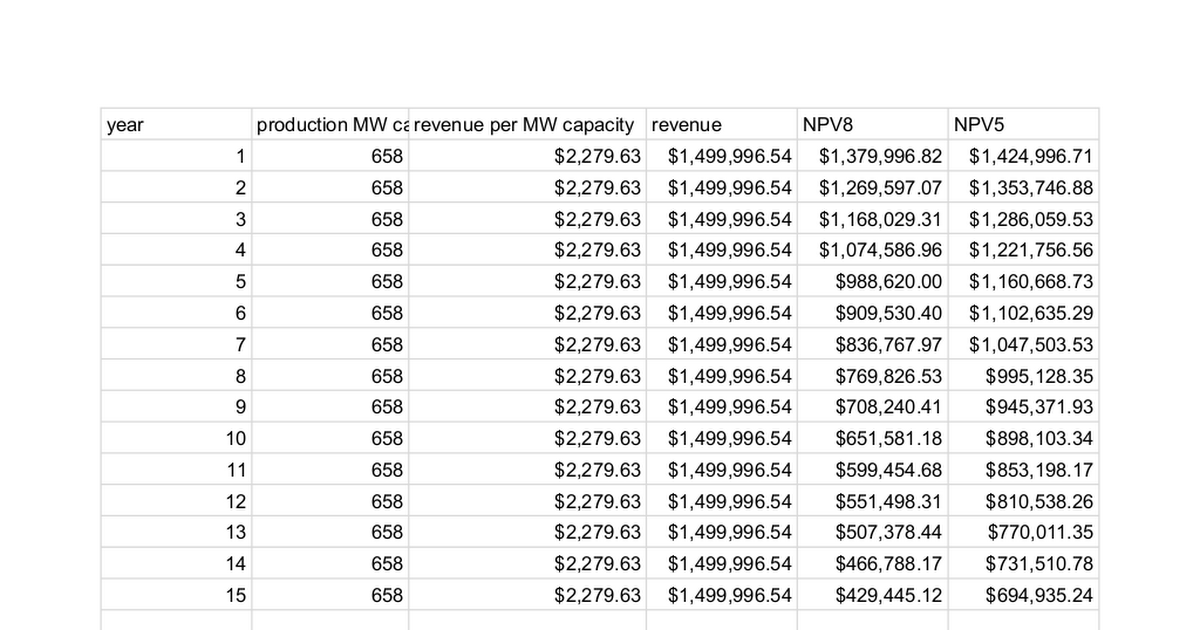

Producing Wind Farm Royalty Economics

There's some lack of details there, what's the expected project life. Are the fixed payments per unit of generation indexed to inflation in any way? So keep in mind this might not be accurate, but I think it's an educated guess.

I modeled it at 15, 20, and 200 year lifetimes. The purchase price is amost exactly the NPV5 of the 20 year project life. If you use the shorter 15 year project life or use a higher discount rate like 8% the expected returns are negative.

As I'm writing this there is a banking crisis where banks are in real trouble for owning long term bonds with low yields. These returns seem very much like long term low yield bonds.

So, what happens if we treat this more as a perpetual asset, in this case with a 200 year lifetime? Well, not much. The NPV8 is still negative to the purchase price in year 200. The NPV5 does a little better, but the simple math is if you discount revenue 21+ years in the future to today it's not worth very much today.

It seems like this royalty just locks in low returns without upside. Maybe it's low risk, but it's probably not getting good returns on capital and the optionality is poor.

Speculation On Why

Royalty Finance is kind of like being a specialty bank. When someone like Franco Nevada gives royalty financing to a miner they also bring technical and other industry expertise that a normal bank can't match. The number of companies that have both the money and the expertise is small so the deals are less competive. In contrast most banks in the US would lend debt to a solar or wind farm. The solar/wind companies can generally issue bonds or equity on good terms. Their cost of capital is low and there are lines of capital providers lined up to give it to them. They might sign a long term power purchase agreement with a utility company that reduces their market price risk.

If Altius comes in and gives a wind farm a royalty financing deal it probably doesn't mean this wind farm is particularly great compared to the average wind farm. Altius probably isn't turning down deals from dozens of poor quality operating wind farms looking to raise cash and only picking the cream of the crop.

In this case also Altius isn't getting a percentage of the revenue, so they aren't taking risk in the market price of electricity going up or down. That sounds good, more predictable is good for Altius, but it also means they aren't getting paid to take that risk, reducing their returns.

Speculation On Where Upside Might Be

Let's theorize on where we might be able to find value in wind/solar farm royalties, and then we can start looking at projects that match this criteria and see if the returns might be better. After all, maybe Altius is intentionally buying low return cashflowing royalties to anchor the business and allow them to also take on high return but riskier assets.

Closer To Retirement

If we assume a 20 year equipment life for wind/solar and a project has been in operation for say 8-15 years already so it only has 5-12 years of project life left, and you can finance based on that life, well the present value of the equipment upgrade is actually really good.

Earlier Stage

You probably get better terms for taking more risk if you get a royalty on a development stage wind/solar farm. You could also just go to ranchers in west texas near high voltage lines and buy exploration stage royalties before project developers even knocked on their doors. Maybe you could partner with a project developer or start one internally that developed projects and sold them off to operators but kept a royalty. Or you could go to the ranchers getting paid to have windmills on their ranch and buy that revenue stream from them.

Market Pricing

Prices of electricity go up and down minute by minute. There's a lot of risk there. If the royalty is based on revenue, and that revenue is tied to market pricing rather than long term purchase agreement, then the royalty company is taking pricing risk alongside the generator. Over a project life inflation probably is a net benefit to the royalty company then as electric prices come up over time. They also probably get to price the deal based on a concervative price of electricity and then if the expected case plays out see the difference as upside.

Expansion Potential

Maybe there is a solar/wind farm on 100 acres, but the company owns another 400 acres adjacent to it. Buy a royalty on the whole 500 acres, but price it based on the production from the existing 100. If more capacity gets added on the additional land it's all upside to the royalty company.

Full Disclosure

At the time of writing I don't own any shares of Altius.