Valuing Royalty Companies - Anglo Pacific Group

With the change in the Queensland Coal Royalty scheme I thought it would be worth trying to put a value on Anglo Pacific Group.

Overview

Based on a closing price of 152.00 $APF.L has a market cap of $337.77m GPB. Add in debt and it has an enterprise value of $411.88m GBP, which is $505m USD give or take. I put the fair value of their assets at $596.6m USD below. $80m or so of that is the inrease of their royalties from the recent Queensland changes to Kestral. That's a 15% bump in my esitmate of their asset value and the market only gave them a 5% bump in share price. Relative to their assets they seem fairly valued to my eye, but more attractive than they were a week ago.

Subjectively they seem to have very solid assets, but I don't see as much upside optionality as I would like. The market does like cashflow and the second half of 2022 will likely deliver a lot of cashflow, especially from Kestral, so it could be a smart 6-9 month trade. But if you start looking out into 2023 and 2024 the market might not appreciate the cashflow declines.

DCFs and Pre-Production Royalties

It's interesting to see how Anglo's accountants value pre-production assets like Piauí and Dugbe 1 where they apply a probability of commerical production and a discount rate and do a discounted cash flow analysis (DCF).

Let's look at Dugbe 1. They use a chance of commerical production of 25% (down from 75% in 2020), a start date of commerical production of 2030 (unchanged from 2020), a discount rate of 21.5% (improved from 30% in 2020).

Let's just say that the chance of accounting shennagins being afoot are greater than zero. If your chance of commercial production dropped that dramatically why did your discount rate get better? Is it because the two are roughly offsetting so you don't have to make a big accounting value change?

But let's assume these are honest assesments. If we had 4 projects like this we would expect over the next 8 years that 3 of them would have their chance of commerical production go to 0% and one of them have their chance of commerical production go to 100%. That's what a 25% chance of commercial production does to 4 projects. In those 8 years the one project would have appreciated 474% from the discount rate passing (1.215^8) and would have increased 400% from the probability of success quadrupling (100%/25%). Combined that's 1899% gain (474.9% * 400%). We can subtract 300% for the three failed ones, so net 1699% gain. That's about a 42% annualized return. That also assumes that the mines just run off their mine plan without converting any more ounces from lower categories or discovering any more ounces. As we've seen time and time again mines in production will replace at least some of what they mine through exploration.

If we really believe our chance of commerical production is accurate we should not double penalize the project with a higher discount rate, because we already penalized it with the chance of commercial success. So what happens if we use an 8% discount rate instead of the 21.5% discount rate? Well, it's 8 years to start of production, and mine life of 14 years gives an average weighted time from start of production of 7 years.

(.92^(8+7))÷(.785^(8+7)) = 1080%

So the present value of $1.4m carrying value would actually be $15m.

I'm not saying let's 10x all valuations of all Anglo Pacific's pre-production royalties. I'm saying DCF's are only as good as their inputs and it's pretty easy to game them for things far in the future with high degrees of uncertainty. Small changes to cashflows from studies, discount rates, timelines, or chances of commercial production have huge impacts on value.

Assets

| Project | Value |

|---|---|

| Kestral | $203m |

| Voisey Bay | $205m |

| Mantos Blancos | $75m |

| Maracás Menchen | $34 |

| EVBC | $30m |

| LIF | $24m |

| Piauí | $10m |

| Four Mile | $3m |

| McClean Lake | $2.5m |

| Incoa | -$5m |

| Dugbe 1 | $15m |

| CAÑARIACO | |

| RING OF FIRE | |

| Railway | |

| Total | $596.5m |

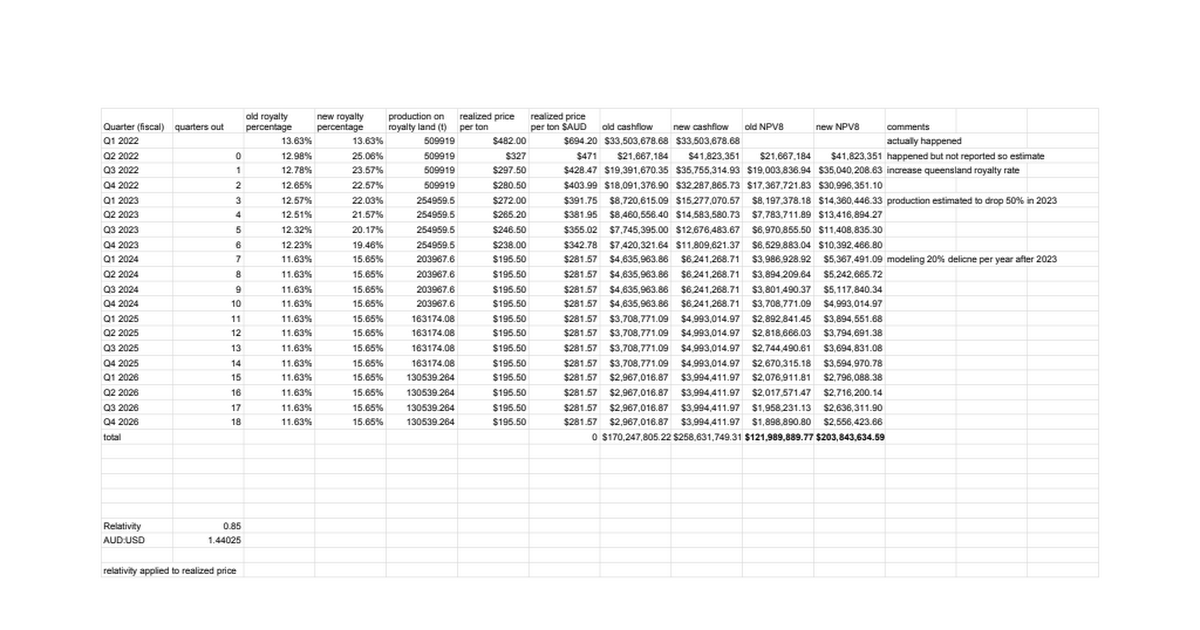

Kestral

2022Q1 they had revenue of $33.5m at $482/t. So 69,502 tons to them. At the current royalty rate of 13.63% that means production on their royalty area was 509919 tons.

They expect a 50% step down in volumes in 2023 vs 2022.

I went ahead and projected the forward met coal futures curve with 85% realized price and a 20% decline in production in 2024, 2025, & 2026 and no production thereafter. Using an 8% discount rate gives an NPV8 of $203m. Is this correct, no way. Who knows what the production rates will be or the realized price. But this is as good of a guess as any.

Voisey Bay

At closing in May 2021 they paid $205m and Cobalt prices are higher now then they were then. So that's a decent number to value it at.

Last quarter with unusually high Cobalt prices the contribution was $6.7m, which annualized would be $26.8m. Put a 10x multiple on that and it would be $268m.

There's a lot of moving parts here, over time their payment percentage on the stream goes up from 18% to 22% and the percentage of cobalt streamed goes down by half. Voisey Bay is transitioning from open pit to underground, and ramping underground.

I'll just take the shortcut and say this is worth what they paid for it.

$LIF.TO

I really like Labrador Iron Ore Royalty Company. It's a high quality long life project that benefits from a shift to low carbon steel. The company has a mix of royalty on revenue and profit share of the mine.

However, for this valuation I'll just value the shares at their current publicly traded market price. If you disagree with that valuation you can add or short an appropriate amount of the stock.

1,032,190 shares * CAD$30.33/share * 0.77 USD$/CAD$ = $24m USD

Mantos Blancos

Purchased for $50.3m in 2019. The copper price was $5700-$6200/ton, well below current levels even with the copper pullback. Total payable copper volumes were 41.3Kt in 2020, 45kt in 2021. They are currently doing upgrades to expand production from 4.3Mtpa to 7.3Mtpa in 2022. Are targeting 55kt production in 2024. IThey are working on a PFS to expand production from 7.3 Mtpa to 10Mtpa, targeting 80kt production of copper.

Of course lower copper prices and increased royalties from the government of Chile might delay capital investments.

1.525% NSR.

50kt/year * 0.01525 * $8000/t = $6.1m/year

80kt/year * 0.01525 * $10,000/t = $12.2m/year

Put a 10x multiple on that and you get a range of $61m-$122m valuation. They have a 20 year mine life at 80kt/year.

Looking just at resources there is 1571kt Cu in M&I. 1571kt * 0.01525 * $8000/ton = $191m

$50.3m, $61m, $122m, $191m. That's a big range. I'm going to call it $75m because I think we have pretty near term visability to that based on expanding capacity and current copper prices.

Maracás Menchen

I don't buy the whole Vanadium battery story. But Vanadiaum is a great steel additive.

20 year mine life. 2% NSR. 12-13kt production estimated in 2022.

Income was $3.4m in 2021. 2022 should have 20-30% increased volumes, but will likely be offset by decreased spot price. Let's just 10x multiple on last year's revenue = $34m.

Four Mile

1% NSR on a Uranium mine. There's a lawsuit. Still, $300k/yr is $300k/yr. Call it a 10x multiple $3m valuation.

McClean Lake

It's a weirdly structured loan. But accountants probably value loans about right, so $2.5m carrying value.

EVBC

2.5% NSR on gold, 3% when gold over $1,100/oz. A Spanish Copper/Gold mine near end of life. Cashflowed $3.0m in 2020, $3.2m in 2021, 2022 projected to have similar gold production. Only 6.5year of mine life based on reserves, but 24 years based on M&I resources.

Spain is a pretty awful jurisdiction, corrupt, high energy prices, hard permitting. But it's in operation.

1.205Moz Au in M&I.

1205000 oz * 0.03 * $1826/oz = $66m

10x $3m annual revenue = $30m.

Carrying value on the balance sheet is $13.9m

I'd give it $66m if it is was a better jurisdiction, but its not, so I'll only give it $30m based on revenue. I think the accounting carrying value is too concervative.

Piauí

A nickel project in Brazil. Heap-leach. Basically a small hill (72 million tons) has 1% nickel and trace cobalt. Expanding demonstration plant. They have a 1.25% GRR. But they also have the right to invest $70m to up it to 4.5% after some milestones are met (presumably the bankable feasability study gets completed).

As at 31 December 2021 the Group assessed the probability of the Piauí project reaching commercial production at 90% in relation to the

start-up plant and 25% in relation to expansion project (2020: 25% start-up and 25% expansion project) and applied this to the discounted

future cash flows of the royalty with a 13.50% (2020: 13.50%) pre-tax nominal discount rate, resulting in a valuation of $5.4m (2020:

$2.1m). The $3.3m increase in carrying value has been recognised as a royalty financial instrument valuation gain in the income

statement for the year (2020: $0.5m increase)

Carrying value on their accounting is $5.4m. They originally paid $2m and it's clearly increased in value through permitting, updated JORC resources, demonstration plant, etc. I feel like the carrying value is probably understating the value here. But it's hard to say because there is a very high chance they put $70m more into this and completely change the value. My back of the napkin math says that would be a good investment. The carrying value gives no credit to the investment option.

Let's pull a magician and pull a number out of a hat. $10m.

Incoa

They have to contribute $20m to earn 1.23% GRR on a Clacium Carbonate project.

After funding, the Group anticipates receiving average annual cash flow of approximately $1.75m to $2m over the first 10 years, and approximately $2.75m to $3.0m per annum longer term over the life of the project (in real terms).

That doesn't exactly seem amazing. The top end of the cash flow would give a 10 year payback. If you assume a 20 year mine life and midpoint of the cashflow at $1.875m in years 1-10 and $2.875m in years 11-20 you get an NPV8 that is amost exactly $20m. That's pretty poor returns for a lot of risk and cost of capital.

This annoys me. I'm going to carry it at -$5m despite the basically breakeven NPV8 to penalize them for the opportunity cost.

Dugbe 1

Carrying value by the accountants is $1.4m. I kind of beat the dead horse as to why that is suspect in the introduction.

The net smelter return royalty over the Dugbe 1 project is classified as FVTPL as outlined innote 5. As at 31 December 2021 the Group

assessed the likely start date of commercial production at Dugbe 1 to be 2030 (2020: 2030), and applied a 25% (2020: 75%) probability

factor to the project reaching commercial production to the discounted future cash flows of the royalty with an 21.50% (2020: 30.00%)

pre-tax nominal discount rate, resulting in a valuation of $1.4m (2020: $1.1m). The $0.3m increase (2020: $0.3m increase) in carrying

value has been recognised as a royalty financial instrument valuation gain to the income statement for the year

3.3Moz M&I, 2% NSR. If in production that would be worth

3,300,000 * 0.02 * $1826 = $120m.

Figure 8% discount to 8 years into production 50% discount (0.92^8 = 0.51). 25% chance it actually makes it to production.

$120m * 0.5 * 0.25 = $15m present value, which happens to be the 8% discount version of their DCF carrying value as explained in the introduction.

Pasofino Gold did a final feasability study June 13. The market cap of Pasofino Gold, which owns 49% of the project and nothing else, is CAD$28.7m. So 100% of the equity in the project would be worth $58.5m. The pre-production capex is $379m. Add them together and the project is being valued by the market at roughly $437.5m. Using our NSR to profit table from earlier

We get 2% NSR as being equivalent to 15.2% of mine profit, or about $66m. So the equity says we aren't crazy for thinking $15 is a sane valuation. Though I think the equity is overly optimistic.

Now, is 25% really the chance this becomes a mine? I don't know. Liberia isn't exactly a tier 1 jurisdiction, you have to cut down a lot of forest (no environmental permit yet), you have to resettle some local residents, you have to actually finance it or sell your company to someone who can. It has a high strip ratio and relatively low grade for a CIL plant. But it's open pittable and there's a lot of it, big open pit projects are pretty popular.

If this were a big part of Anglo's value I would spend a LOT of time estimating the chances this becomes a mine, but it isn't so I won't. $15m lottery ticket worth $0 or $60m, who knows.

Full Disclosure

I don't have a position in Anglo Pacific Group, but continue to follow them for potential investment as I love the royalty model and appreciate their approach to putting together royalties on diverse commodities.